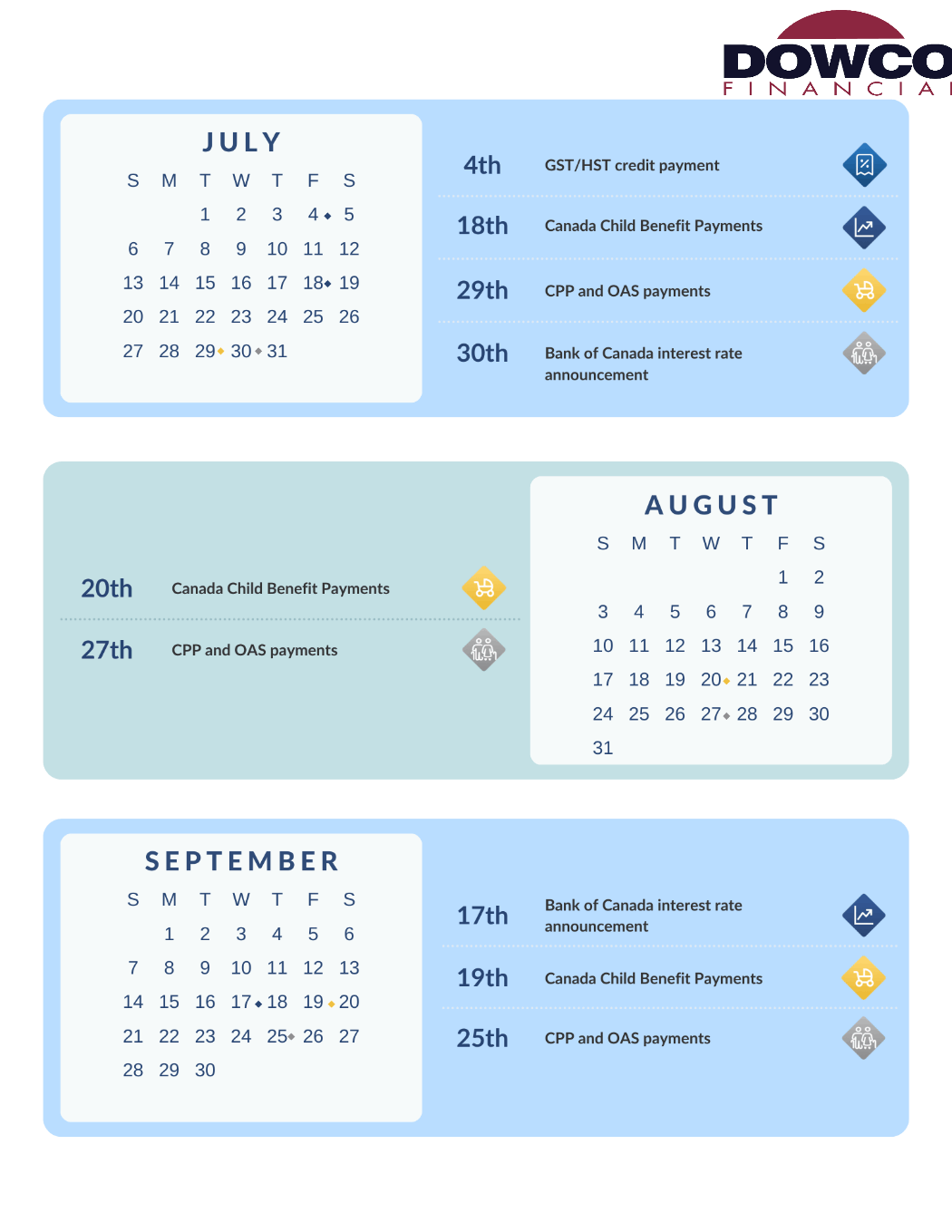

Choosing A Group Benefits Provider

What to Look for in a Group Benefits Provider (and How We Help Employers Get It Right)

If you’re reviewing your group benefits plan—or starting one for the first time—you’ve likely realized how overwhelming it can be to compare providers. At our firm, we work with employers across Canada to help them make informed, confident decisions about their benefits programs. And if there’s one thing we’ve learned, it’s this: the lowest quote doesn’t always mean the best value.

As independent group benefits specialists, our job is to guide you through the process, simplify your options, and build a plan that fits your business and your team.

Here are five key things we help employers evaluate when choosing a group benefits provider:

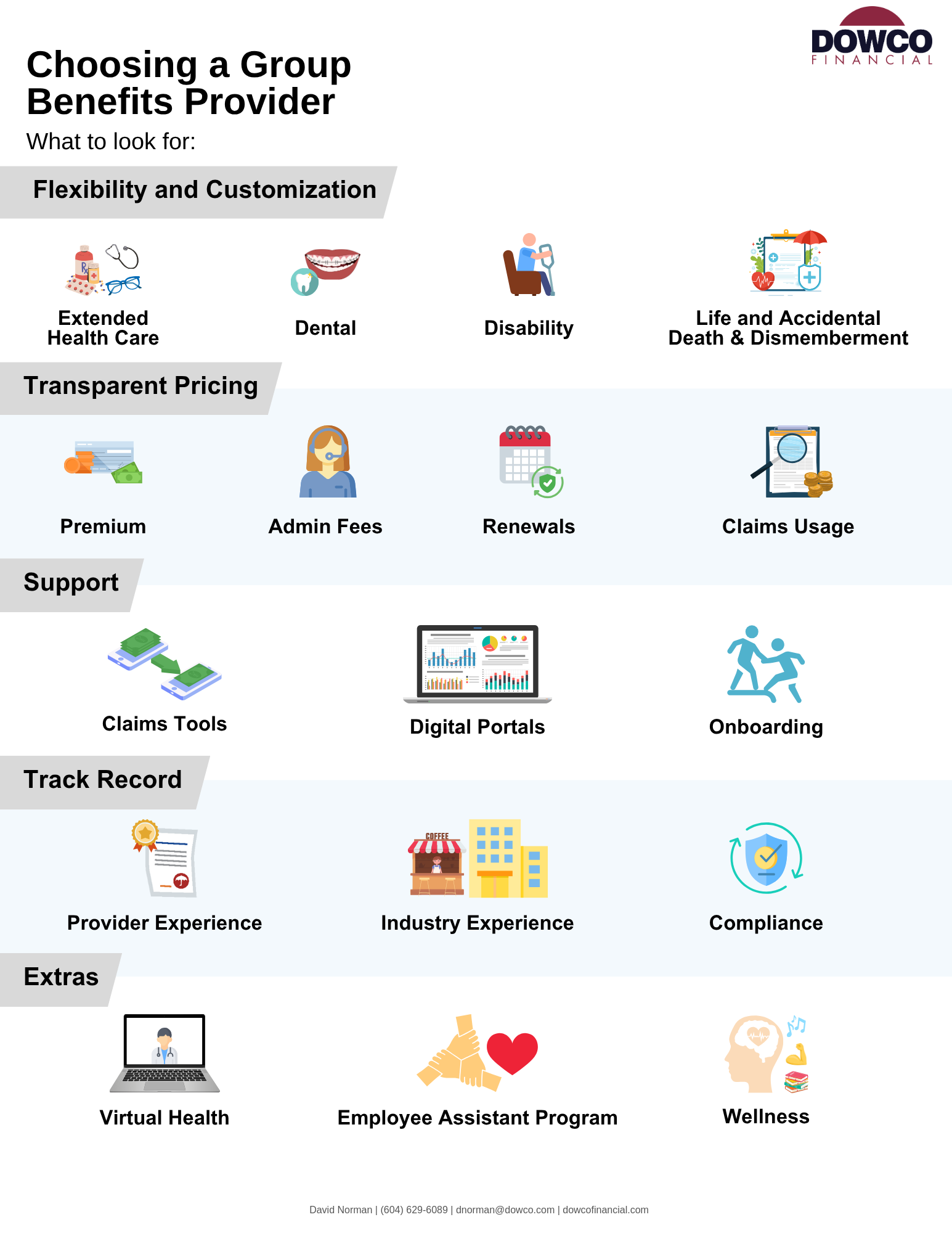

1. Flexibility and Customization Are Essential

No two businesses are the same. That’s why we work with providers that offer modular, customizable plans. Whether you’re scaling up, restructuring, or maintaining a lean team, we’ll help you find the right mix of core and value-added benefits.

We typically break benefits into three key categories:

Core Health Coverage

- Extended Health Care: prescription drugs, vision, and paramedical services like physiotherapy or massage

- Dental: including basic, major restorative, and orthodontics

- Disability Insurance: both short- and long-term income protection

- Life and Accidental Death and Dismemberment (AD&D) Insurance: Offers life insurance coverage for employees and their dependents, along with AD&D benefits in the event of a severe injury or accidental death

Additional Benefits

- Critical Illness Insurance: lump-sum coverage for specified serious health conditions

- Emergency Medical Travel Insurance: protection while traveling outside Canada

- Health Spending Accounts and Wellness Spending Accounts

- Employee Assistance Programs

We tailor your plan based on your budget, team needs, and industry benchmarks¹.

2. Transparent Pricing and Clear Expectations

We help you make sense of what you’re really paying for. When we review provider proposals with our clients, we break down:

- Premium costs and rate structures

- Admin and service fees

- Renewal practices and what drives pricing changes

- Claims usage and cost control opportunities

As your partner, we advocate for your best interest and help avoid surprises at renewal².

3. Strong Support for Your Team and Admin Staff

We only recommend providers that make life easier for both your employees and your internal team. That includes:

- Mobile and desktop-friendly claims tools

- Clear digital portals for both employees and plan administrators

- Helpful onboarding and documentation

We also provide ongoing support after implementation—especially during renewals or changes in your workforce.

4. A Trusted Track Record in the Canadian Market

We’ve worked with a wide range of providers over the years and have seen firsthand what sets the best apart. When we evaluate who to recommend, we draw on both our industry knowledge and direct client experience. We look at:

- Their track record serving Canadian businesses across various regions

- Their ability to support companies in your specific industry or business size

- Client references, satisfaction feedback, and third-party reviews³

- Consistent alignment with provincial and federal compliance requirements

Our recommendations are based on what we’ve seen work—not just what’s on paper. We only suggest providers who’ve proven themselves reliable, responsive, and supportive in real-world situations.

5. Extras That Truly Support Employee Wellbeing

Benefits plans aren’t just about insurance anymore. We help you evaluate added features that can increase employee engagement, including:

- Virtual healthcare and mental health tools

- Employee Assistant Programs with access to counselling and wellness resources

- Financial wellness programs

Employers that prioritize wellbeing tend to see stronger engagement, lower absenteeism, and improved workplace culture⁴.

Let’s Build a Plan That Works

As independent group benefits specialists, we’re not tied to any one provider. That means we work for you, not the insurance company. Our role is to simplify the process, compare the best options, and help you build a benefits program that supports your people—and your business.

Whether you’re starting fresh, reviewing your current plan, or just want a second opinion, we’re here to help.

Let’s talk.

We’d love to learn more about your team and walk you through how we can help you build a benefits plan that fits—now and as you grow.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice. Always consult a qualified professional regarding your specific situation. We are not responsible for any actions taken based on this content.

Sources:

- Canadian Life and Health Insurance Association. Employee Benefits: CLHIA. CLHIA, 2023, www.clhia.ca/web/CLHIA_LP4W_LND_Webstation.nsf/page/EmployeeBenefits.

- Financial Consumer Agency of Canada. Financial Literacy for Canadian Business Owners. Government of Canada, 2024, www.canada.ca/en/financial-consumer-agency.html.

- Benefits Canada. Home Page. Benefits Canada, 2025, www.benefitscanada.com/.

- Sun Life. “Sun Life Wellness Report Shows Employee Well-Being Is Key to Business Success.” Sun Life Newsroom, 2023, www.sunlife.ca/en/about-us/newsroom/news-releases/2023/sun-life-wellness-report-shows-employee-well-being-is-key-to-business-success/.

-David-Norman-fHnp3LJtNp4ae97gn.png)

-David-Norman-fHnp3LJtNp4ae97gn.png)