Tax planning is an essential part of managing your money – both while living and after your death. You want to maximize the amount of money to your beneficiaries, not the government. We have three tips to help you reduce taxes on your hard-earned money:

Make the most of the lifetime capital gains exemption

Decrease your end-of-life tax bill

Look into Immediate Financing Arrangements

Lifetime capital gains exemption

The good news is that you can save a lot of money on taxes using the lifetime capital gains exemption. The bad news is that you could lose out on some of those savings unless you follow all the appropriate steps. Having a financial team to guide you through these steps is essential. When it comes to selling all or part of your business, your lawyer, accountant, and financial advisor must be all on the same page.

End-of-life tax bill

As with the lifetime capital gains exemption, working with your financial team to ensure your affairs are in order is crucial. Without the proper paperwork, your hard-earned money may not go to the family members, friends, or charities you want to support. Take the time to ensure that your wishes are properly documented and that you have filled out all essential paperwork.

Consider an Immediate Financing Arrangement

An Immediate Financing Arrangement (IFA) lets your business:

Get a life insurance premium on behalf of a shareholder

Create a tax deduction

Transfer assets tax-free from the business to a shareholder’s estate

Also, you can use an IFA to help increase your business’ cash flow by pledging the life insurance policy as collateral for a loan. The loan can be invested into the business or other investments if the company does not need the additional cash flow.

The Takeaway

While this can all seem overwhelming, it is essential to make sure you take the proper steps to protect your business and minimize your tax bill. But you don’t have to do this alone – contact us today for expert advice and guidance.

https://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2022/07/Dont-lose-all-your-hard-earned-money-to-taxes.png?time=1714369023300500Dowco Financialhttps://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2019/12/dowcoEnfold.jpgDowco Financial2022-07-05 06:00:002022-07-05 12:18:52Don’t lose all your hard-earned money to taxes

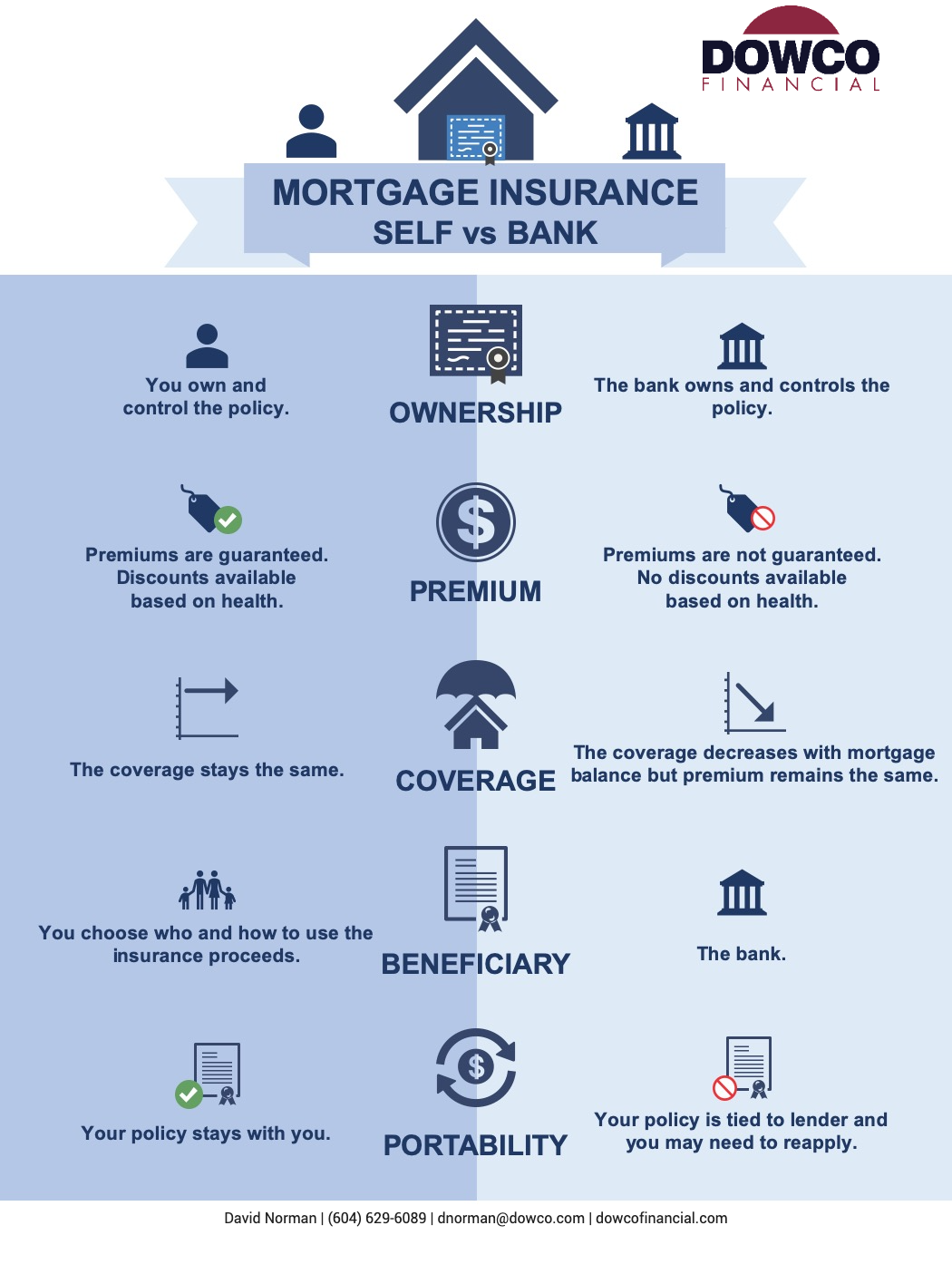

Before buying insurance from your bank to cover your mortgage, understand the difference between self owned mortgage life insurance and bank owned life insurance. The key differences are ownership, premium, coverage, beneficiaries and portability.

Ownership:

Self: You own and control the policy.

Bank: The bank owns and controls the policy.

Premium:

Self: Your premiums are guaranteed at policy issue and discounts are available based on your health.

Bank: Premiums are not guaranteed and there are no discounts available based on your health.

Coverage:

Self: The coverage that you apply for remains the same.

Bank: The coverage is tied to your mortgage balance therefore it decreases as you pay down your mortgage but the premium stays the same.

Beneficiary:

Self: You choose who your beneficiary is and they can choose how they want to use the insurance benefit.

Bank: The bank is beneficiary and only pays off your mortgage.

Portability:

Self: Your policy stays with you regardless of your lender.

Bank: Your policy is tied to your lender and if you change, you may need to reapply for insurance.

We’ve created an infographic about the difference between personally owned life insurance vs. bank owned life insurance.

https://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2022/06/mortgageLifeInsurance.jpg?time=1714369023405720Dowco Financialhttps://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2019/12/dowcoEnfold.jpgDowco Financial2022-06-02 06:00:002022-06-02 13:08:54The Best Way to Buy Mortgage Insurance

For a long time, there were limited options for most investors. But now, there are hundreds of investments for investors to choose. However, this amount of choice can be overwhelming. Fortunately, an investment advisor can help you figure out what the right investment choices are for you.

Meeting your investment advisor

When you first meet with your investment advisor, they will tell you about their obligations and responsibilities. They should:

Give you general information about your various investment choices (e.g. stocks, bonds, mutual funds)

Tell you how they are compensated for their services

Ask if you have any questions about specific investment vehicles (such as RRSPs or TFSAs)

Determining your goals and expectations

The next step is to for your investment advisor to fill out a “Know Your Client” type of worksheet. The information on this worksheet will help your investment advisor determine the most suitable investment options for you. You’ll need to provide information on your:

Income

Net worth

Investment knowledge

Risk tolerance

Time horizon (how long you want to invest for)

How frequently do you want to invest

Developing your investment plan

Once they have all the information they need, your investment advisor will suggest the investments they think are appropriate for you.

Implementing the plan

Once you approve your investment advisor’s suggestions, you will fill in all the appropriate paperwork to set things in motion. After that, you must provide a way to fund your investments. Your investment advisor can then make any initial purchases and set up any ongoing fund purchases or transfers from other investments.

Monitoring the plan

Your investment advisor should contact you at least once a year to make sure your plan is still suitable for you and discuss any changes you want to make to it. If you have any major life events, such as getting married or changing jobs, you should contact your investment advisor to see if you should revisit your plan.

The sooner you start your investment planning, the sooner you can reach your investment goals! So contact us today!

https://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2022/05/The-Five-Steps-to-Investment-Planning.png?time=1714369023281500Dowco Financialhttps://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2019/12/dowcoEnfold.jpgDowco Financial2022-05-01 06:00:002022-05-01 11:44:08The Five Steps to Investment Planning

On April 7, 2022, the Federal Government released their 2022 budget. We have broken down the highlights of the financial measures in this budget into the following different sections:

Housing

Alternative minimum tax

Dental care

Small businesses

Tradespeople

Canada Growth Fund

Climate

Bank and insurer taxes

Housing

There were several tax measures related to housing introduced in the budget.

Budget 2022 introduced a new kind of savings account – a Tax-Free First Home Savings Account (FHSA).

These are the key things you need to know about the new FHSAs:

You must be at least 18 years of age and a resident of Canada to open an account. You must also not currently own a home or have owned one in the previous four calendar years.

You can only open and use an FHSA once, and you must close it within a year after your first withdrawal.

Contributions are tax-deductible, and income earned in an FHSA will not be either while it is in the account or when you withdraw it.

There is a lifetime contribution limit of $40,00, with an annual contribution limit of $8,000. You can’t carry contribution room forward.

If you don’t use the funds in your FHSA within 15 years of opening it, you can transfer them to an RRSP or RRIF tax-free. Transfers to an RRSP do not impact your RRSP contribution room.

Two existing tax credits were increased, and a new one was introduced:

The First-Time Home Buyers’ Tax Credit amount was increased from $5000 to $10,000, giving up to $1,500 in direct support to home buyers. This tax credit applies to all homes purchased on or after January 1, 2022.

The annual expense limit for the Home Accessibility Tax Credit has been increased to $20,000 for 2022 and subsequent tax years.

A new tax credit, the Multigenerational Home Renovation Tax Credit, was introduced, which will start in 2023. This tax credit is a 15% refundable credit for eligible expenses up to $50,000 (maximum tax credit is $7,500) for constructing a secondary suite for a senior or an adult with a disability to live with a qualifying relative.

Budget 2022 proposes new rules, effective January 1, 2023, that anyone who sells a residential property they have held for less than 12 months would be subject to full taxation on their profits as business income. However, there will be some exemptions to these rules due to life events such as a death, disability, the birth of a child, a new job, or a divorce.

Budget 2022 also announces restrictions that would help ensure that Canadians, instead of foreign investors, own housing. A two-year ban will be introduced on non-residents buying residential property, with some exceptions, such as individuals who have work permits and are living in Canada.

Alternative Minimum Tax

In Canada, the top federal tax rate is 33% and starts at an income of $221,708. However, many high-income filers end up paying less tax than this due to tax deductions and tax credits.

The goal of the Alternative Minimum Tax (AMT), which has been around since 1986, is to ensure high-income Canadians are paying their fair share of taxes. However, it has not been substantially updated since it was introduced. In Budget 2022, the government indicated they would be investigating changes to the AMT, which will likely be disclosed in the fall 2022 economic update.

Dental Care

For many Canadians without private coverage, going to the dentist is too expensive. Budget 2022 commits $5.3 billion to provide dental care for Canadians with family incomes of less than $90,000 annually. Coverage will start for children under 12 this year and expand to children under 18, seniors and those living with a disability in 2023, with the program will be fully implemented by 2025.

Small Businesses

Small businesses currently have a 9% tax rate on the first $500,000 of taxable income (compared to the corporate tax rate of 15%). However, after a small business’ capital employed in Canada reaches $15 million, it is no longer eligible for the 9% tax rate.

Budget 2022 proposes gradually phasing out the small business tax rate so that businesses are not discouraged from expanding. The new cut-off for the lower tax rate will be $50 million.

Budget 2022 also includes a proposal to create an Employee Ownership Trust. This would be a new, dedicated trust under the Income Tax Act to support employee ownership.

Tradespeople

Budget 2022 introduces the Labour Mobility Deduction. This would allow eligible tradespersons and apprentices to deduct up to $4,000 a year in eligible travel and temporary relocation expenses.

Budget 2022 also commits to providing $84.2 million over four years to double funding for the Union Training and Innovation Program, which would help 3,500 apprentices from underrepresented groups each year.

Canada Growth Fund

Budget 2022 introduces a new Canada Growth Fund, with the goals of both diversifying our economy and helping achieve our climate goals.

The Canada Growth Fund aims to attract considerable private sector investment, support the restructuring of vital supply chains, and bolster our exports. The Canada Growth Fund will also provide backing to reduce our emissions and invest in the growth of low-carbon industries.

Climate

Budget 2022 continues to confirm the government’s commitment to fighting climate change. It commits $1.7 billion over five years to extend the Incentives for Zero-Emission Vehicles Program until March 2025 and also provides funding to create a national network of electric vehicle charging stations.

Budget 2022 also commits $250 million over four years to support the development of clean electricity, including inter-provincial electricity transmission projects and Small Modular Reactors.

Bank And Insurer Taxes

Budget 2022 introduced a new financial measure called the Canada Recovery Dividend. Banks and insurers will have to pay a one-time, 15% tax on 2021 taxable income above $1 billion. This tax will be payable over five years.

Budget 2022 also proposes increasing the tax rate on income above $100 million for banks and insurers to 16.5% (currently 15% for other corporations).

Wondering How This May Impact You?

If you have any questions or concerns about how the new federal budget may impact you, call us – we’d be happy to help you!

https://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2022/04/federalBudget2022FI.jpeg?time=1714369023281500Dowco Financialhttps://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2019/12/dowcoEnfold.jpgDowco Financial2022-04-08 13:15:432022-04-08 14:02:152022 Federal Budget Highlights

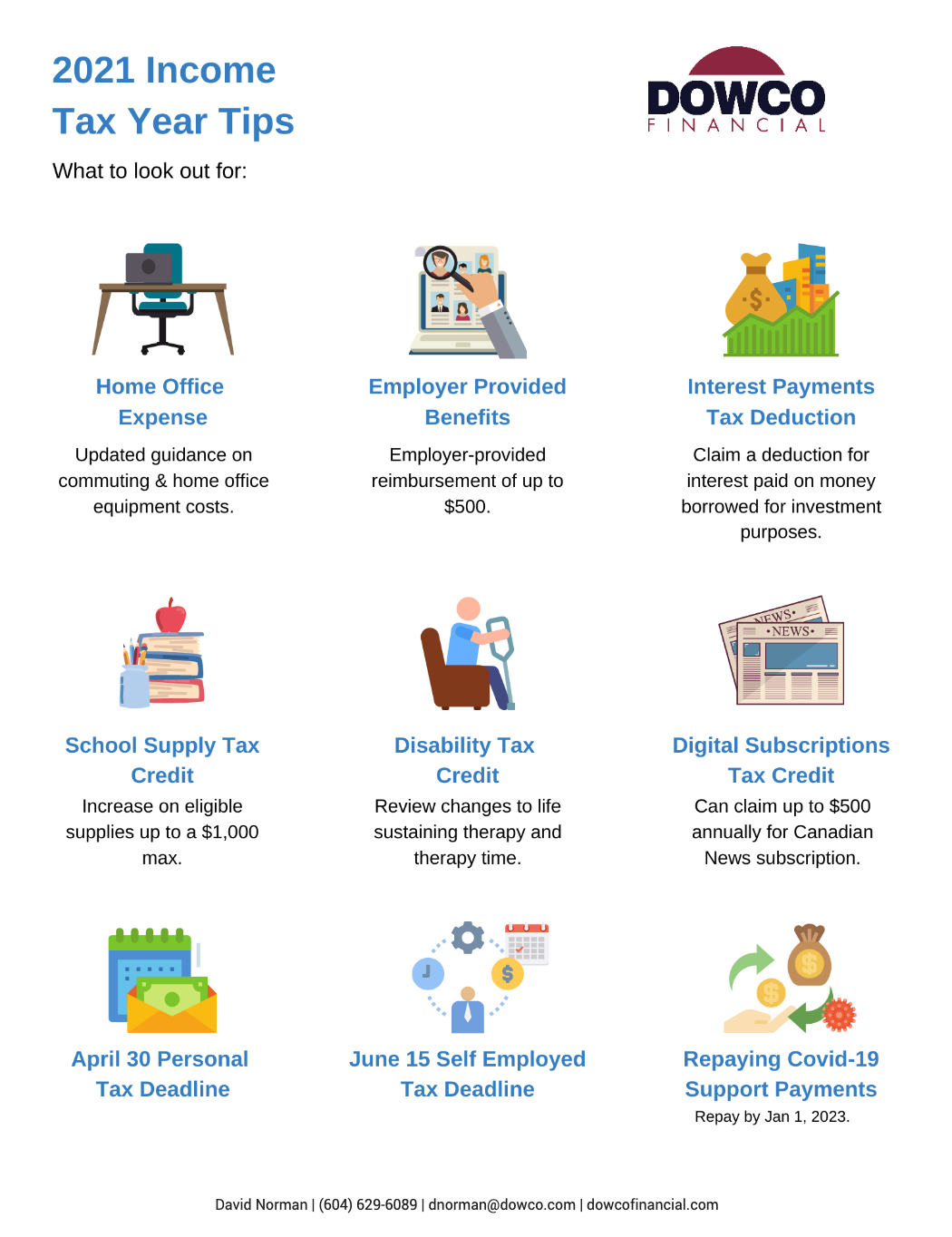

Tax Tips You Need To Know Before Filing Your 2021 Taxes

This year’s tax deadline is April 30, 2022. We’ve got a list of tips to help you save on your taxes!

Claiming home office expenses

You can claim up to $500 under the “flat rate” method if you worked at home due to COVID-19. To claim more, you must use the detailed method to claim home office expenses.

If you repaid COVID-19 benefits, you can deduct the amount on your tax return either for the year you received the benefit or the year you repaid it, or you can split the deduction between both years.

Climate Action incentive can no longer be claimed

As of 2021, this amount can’t be claimed as a refundable credit; instead, you’ll receive quarterly payments via the benefits system.

Disability tax credit(DTC)

If you or a family member are DTC claimants, then you should review the updated criteria for the tax credit in regards to mental functions, life-sustaining therapy and calculating therapy time.

Eligible educator school supply tax credit

This tax credit has been increased to 25 percent for eligible supplies (such as books and games) to a maximum of $1,000.

Tax deduction on interest payments

You can claim a tax deduction for the interest you’ve paid on any money you’ve borrowed to invest. However, you can only do this if you use the money to earn investment income (for example, a rental property).

Self-employed? Be sure to set aside enough for personal income tax!

If you’re self-employed, be sure you put aside enough money (we recommend 25% of your income) to pay your tax bill when the time comes. You’re taxed only on your net income (total income minus expenses).

You need to plan ahead for tax changes if you want to retireabroad

Planning to retire abroad? If so, you need to be aware of the tax implications and plan accordingly. If you sell your house and move, you may be considered a “non-resident” and be subject to capital gains taxes on non-registered investments (even if you have not sold them) or have your pension subjected to a withholding tax.

You can stop making CPP contributions if you’re over 65 but plan to keep working

If you’re 65 and already collecting Canada Pension Plan (CPP) benefits but also still working, you may be able to stop making CPP contributions. To do so, you need to fill in the form CPT30.

Need help?

Not sure if you qualify for a credit or deduction? Give us a call – we’re here to save you money on your taxes!

https://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2022/04/2021-Tax-Tips-Featured-Image.jpeg?time=1714369023281500Dowco Financialhttps://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2019/12/dowcoEnfold.jpgDowco Financial2022-04-01 13:46:592022-04-01 14:21:582021 Income Tax Year Tips

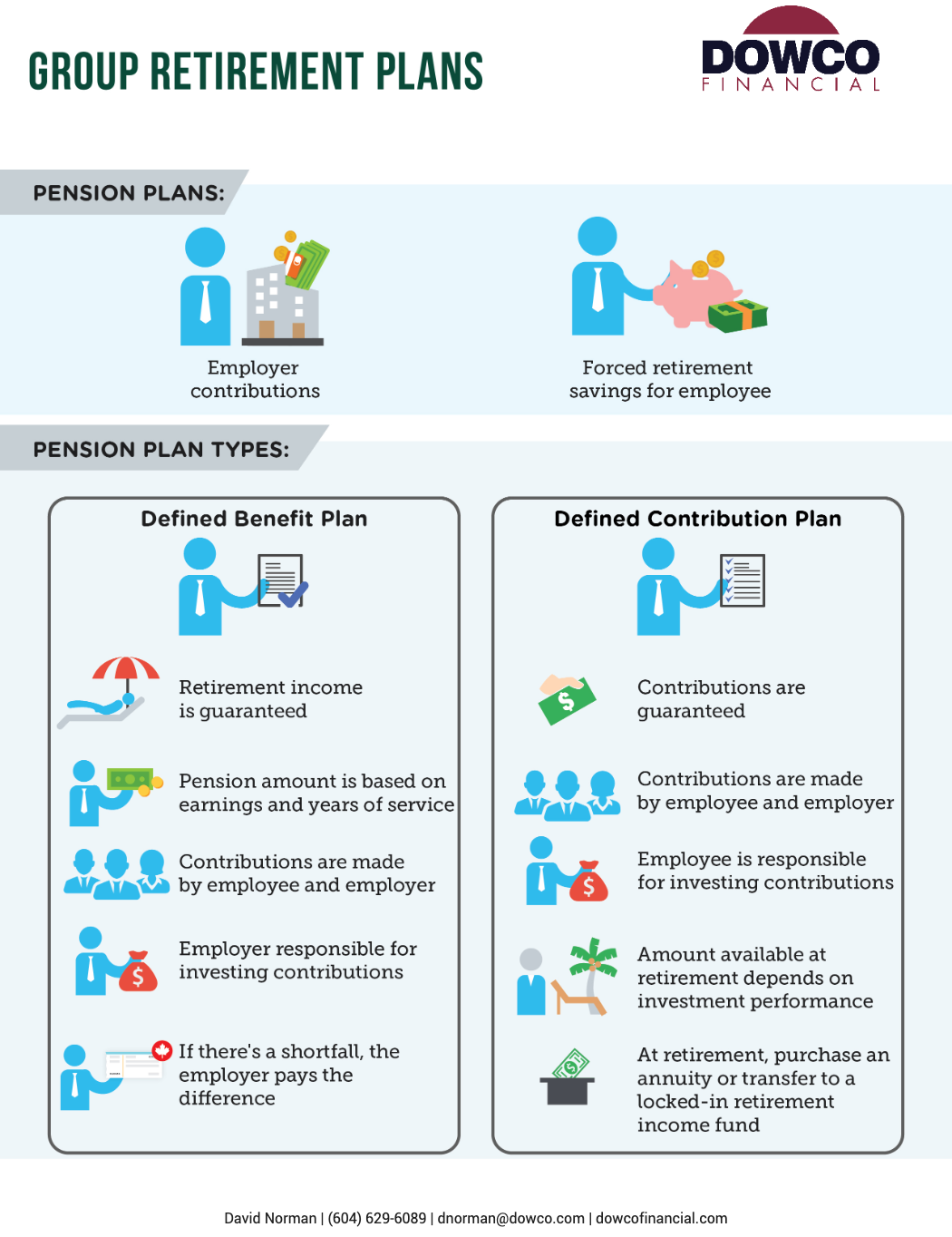

Working at an organization that offers a pension plan is one of the greatest financial advantages a Canadian can enjoy. Pension plans are designed to provide retirement income and help employees reach their retirement goals and for business owners- help retain key employees.

Pension plans can offer:

Employer contributions

Forced retirement savings for employee

There are 2 main types of pension plan:

Defined Benefit Plan

Defined Contribution Plan

Defined Benefit Plan

Retirement income is guaranteed, contributions are not.

The pension amount is based on a formula that includes the employee’s earnings and years of service with the employer

Usually, contributions are made by the employee and employer

The employer is responsible for investing the contributions to ensure there’s enough money to pay the future pensions for all plan members.

If there’s a shortfall, the employer pays the difference.

Defined Contribution Plan

Contributions are guaranteed, retirement income is not.

Usually, contributions are made by the employee and employer.

The employee is responsible for investing all contributions.

The amount available in retirement depends on how the investment performs including total contributions.

At retirement, the money in the account can be used to generate retirement income through purchasing an annuity or transferring the amount to a locked-in retirement income fund.

In summary, a defined benefits plan guarantees you a retirement income and a defined contribution plan guarantees contributions but not retirement income.

In 2015, CIBC conducted a poll to see how many Canadian business owners had a business transition plan. Almost half of them didn’t have one.

No business owner likes to think about handing over their business they’ve built from the ground up. But the fact of the matter is, you will have to do it eventually. Even more concerning, what if you were to become ill or incapacitated? Making a decision of this magnitude during trying times would not be ideal.

Your two main choices for passing on your business are:

Selling it

Transferring ownership to a successor of your choice (this can either be a family member or a non-family member such as a key employee)

When you die, all your capital property is deemed to have been sold immediately before your death. This includes your business. This means that capital gains taxes will be charged on whatever the fair market value (FMV) of your business is considered to be at the time of your death.

The higher the FMV of your business, the higher the capital gains taxes that will be charged. Your successors may not have the funds to pay these taxes which may force them to sell the business in order to fund the tax liability; thus, not to reaping the benefits of all your hard work as intended.

The good news is that there’s a way to protect your business; an estate freeze.

What is an estate freeze?

For the business owner, an estate freeze can be an integral part of your estate planning strategy. The purpose of an estate freeze is to lock-in (freeze) the value of the business, freeing the successor from the tax liability that may arise should the business’ value increase.

This is how an estate freeze works:

As a business owner, you can lock in or “freeze” the value of an asset as it stands today. Your successors will still have to pay taxes on your business when they inherit it – but not as much as if you hadn’t “frozen” your business and your company had increased in FMV.

You continue to maintain control of your business. As well, you can receive income from your business while it is frozen.

Your successor now benefits from the business’ future growth, but they won’t have to pay for any tax increases that occur before they inherit the business.

Freezing the value of your business can help you plan your tax spending properly. Selecting to “freeze” your business can help give you peace of mind that your successors won’t have to spend a considerable part of their inheritance on excessive taxes.

What happens when you freeze your estate?

When you execute an estate freeze, the first thing you need to do is exchange your common shares for preferred shares. Your new preferred shares will have a fixed (a.k.a. “frozen”) value equal to the company’s present fair market value. Make sure you have everything in place to properly determine the fair market value before you exchanging your shares.

Your company will then issue common shares, which your successors subscribe to for a nominal price (for example, 1 dollar). Note that your successors don’t own the stock yet – subscribing to the stocks means they will take ownership of the stocks at a future date.

As part of your estate freeze, you must have a shareholders’ agreement ready to bring in new shareholders. This agreement should list any terms and conditions related to the purchase, redemption, or transfer of your company’s common shares.

1. You can choose to receive some retirement income from your preferred shares by cashing in a fixed amount gradually. This action will reduce your preferred shares’ total value, reducing income tax liability upon death. For example:

Your shares are worth $10,000,000, and you need $100,000 annually. You can then redeem $100,000 worth of shares.

If you live for 30 more after you freeze your estate, you will have withdrawn $3,000,000 of your shares. This reduces the value of your shares to $7,000,000.

At your death, your tax liability is lower than it would have been had your shares remained at the original value of $10,000,000.

2. You can opt to maintain voting control in your company. This can be complicated (so you should consult a licensed professional), but you can set up your estate freeze so that you still have voting control in your business with your preferred stock.

How you can benefit from an estate freeze

You get peace of mind. The most important benefit to a tax freeze is that you know, whoever your successors are, they will receive what they are entitled to and not have to deal with any unpredictable tax burdens. Since an estate freeze fixes the maximum amount of taxes to be paid, you can properly plan how much money to set aside for this tax liability. One option is to have a life insurance policy equal to the amount of the tax liability, with your successor as the beneficiary, so you know they will have enough money to pay for these taxes.

You encourage participation in growing your business. Your chosen successors will be motivated to help the company grow, as they know they will benefit in the future.

Further tax reductions. If your shares qualify for lifetime capital gains exemption, then an estate freeze also helps further reduce your successor’s tax liability.

Is an estate freeze the right strategy for you?

There are a few things you need to consider when deciding if an estate freeze is right for you or not.

Retirement funding. What kind of retirement savings, if any, do you have? If you have money put aside in RRSPs, TFSAs, or even have a pension from a previous job, then an estate freeze may be the right choice for you. If you were planning to sell your company and live off the proceeds in retirement, then it likely is not the right choice for you.

Succession plans. Do you have someone in mind who would be a suitable successor? Just because you think your child, spouse, or best employee may want to take over your business doesn’t mean they do. Talk to anyone you are considering making a successor and see if they are both interested in and able to keep your business going.

Family relationships. Trying to figure out how to select a successor if you have several children may be challenging. It can cause a lot of strain amongst your children if they are all named successors if only some of them are actively interested in running the business. You may want to consider only making one child a successor and providing for your other children in different ways, such as making them a life insurance beneficiary.

If you decide to pursue an estate freeze for your business, you are helping plan for your heirs’ future and cutting down on the amount of taxes that will eventually have to be paid. That being said – an estate freeze can be complicated, and all the steps must be performed correctly. Be sure to consult an experienced professional be taking any steps to freeze your estate.

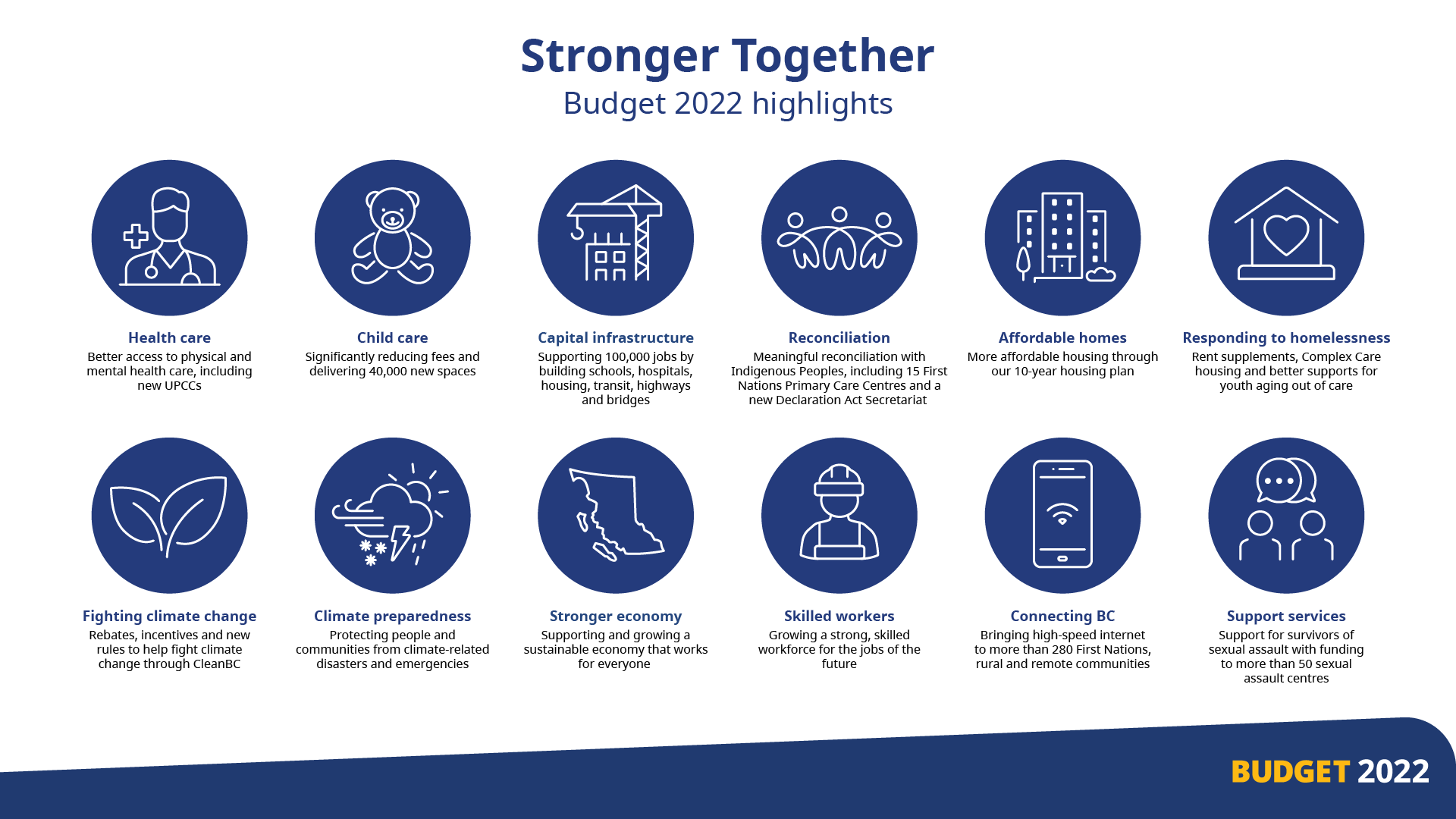

On February 22, 2022, the B.C. Minister of Finance announced the 2022 budget. We have highlighted the most important things you need to know about this budget.

Budget 2022 contains several measures to help build a more robust economy, including $50 million to support growing sectors such as life sciences, manufacturing, and agriculture. In addition, the budget allocates funding to help industries impacted by COVID-19, including the tourism industry, the arts, and non-profit organizations. Budget 2022 supports workers looking to upgrade their skills or train for new jobs, with an emphasis on providing training for early childhood educators and health care assistants.

Offering Stronger Health Care

Budget 2022 includes funding to support the opening of new Urgent and Primary care centres and continuing Pathway to Hope from Budget 2021, which dedicated $500 million over two years to support mental health and addiction care. As well, Budget 2022 includes funding for B.C. Centre for Disease Control.

Expanding Child Care Options and Lowering Fees

Working with the federal government, the B.C. government will create 40,000 new licensed child care spaces for children under six over the next seven years. The budget also includes an investment in increasing before and after school spaces and expanding the Seamless Day program to include 44 school districts.

Fees for full-day infant and toddler care will be reduced by 50% by the end of 2022 (to an average of $20/day). Average preschool and before and after school care fees will be cut to less than $20/day for the 2023/2024 school year.

Supporting Capital Infrastructure

Budget 2022 commits to spending over $27 billion to support critical infrastructure, including schools, hospitals, affordable housing, and highways and bridges. This amount of capital spending will support the creation of over 100,000 jobs.

Providing Funding For Affordable Homes

Budget 2022 allocates 2 billion dollars to HousingHub. HousingHub is a program that provides low-interest loans to private developers and other community groups and is designed to give middle-income British Columbians more opportunities to rent or own homes.

Promoting Clean Transportation

Budget 2022 continues to build on the B.C. government’s plan to fight climate change. PST will no longer be charged on used Zero-Emission Vehicles (ZEVs). The luxury tax threshold on ZEVs has been increased, and rebates will be available for both ZEVs and ZEV charging infrastructure.

No Changes To Corporate or Personal Tax Rates

Budget 2022 does not include any changes to the province’s corporate tax rates or personal tax rates.

We can help!

We can help you assess the impact of this year’s budget changes on your finances or business. Give us a call today!

https://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2022/02/bcBudget2022.png?time=171436902310801920Dowco Financialhttps://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2019/12/dowcoEnfold.jpgDowco Financial2022-02-23 09:40:272022-02-23 09:54:282022 British Columbia Budget Highlights

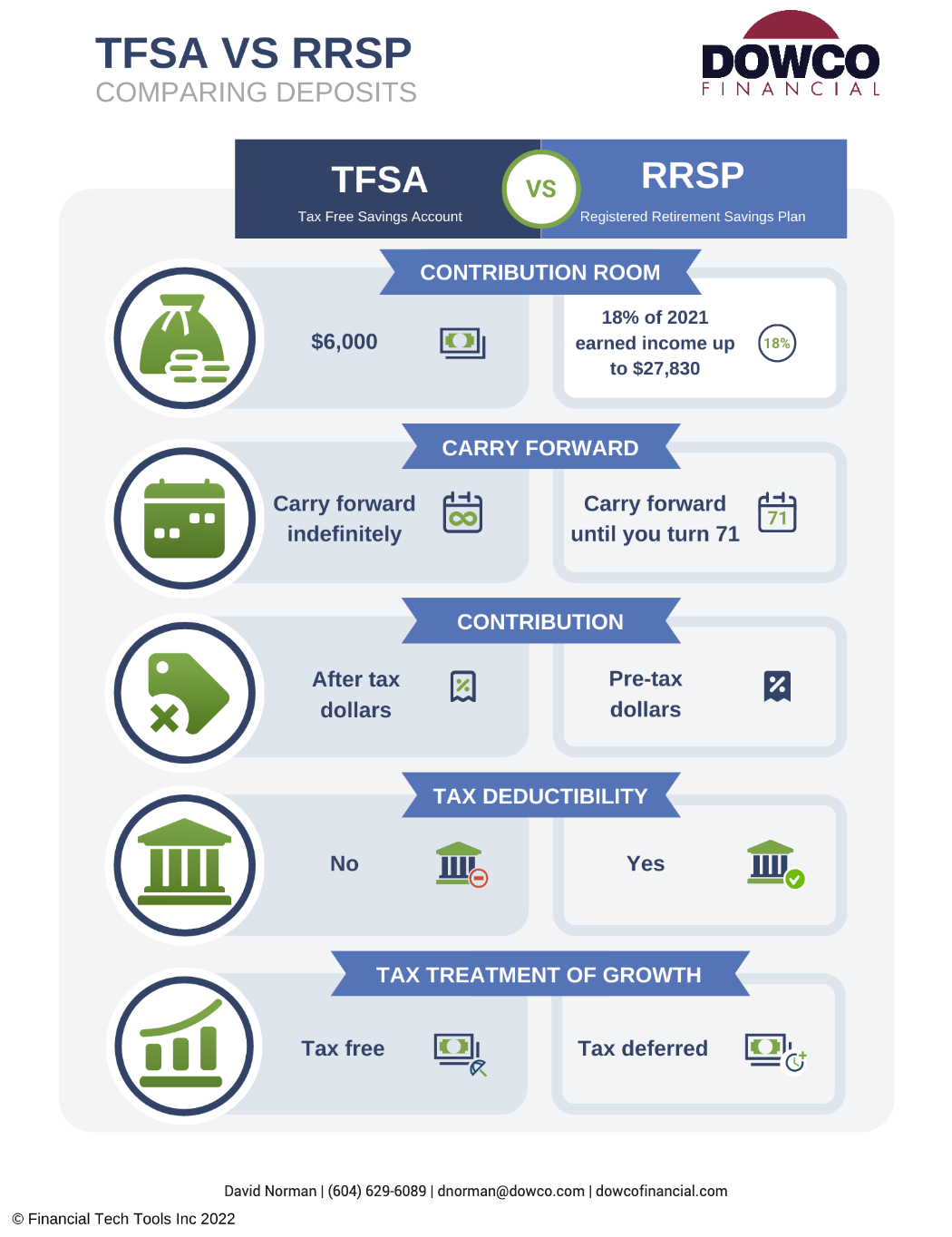

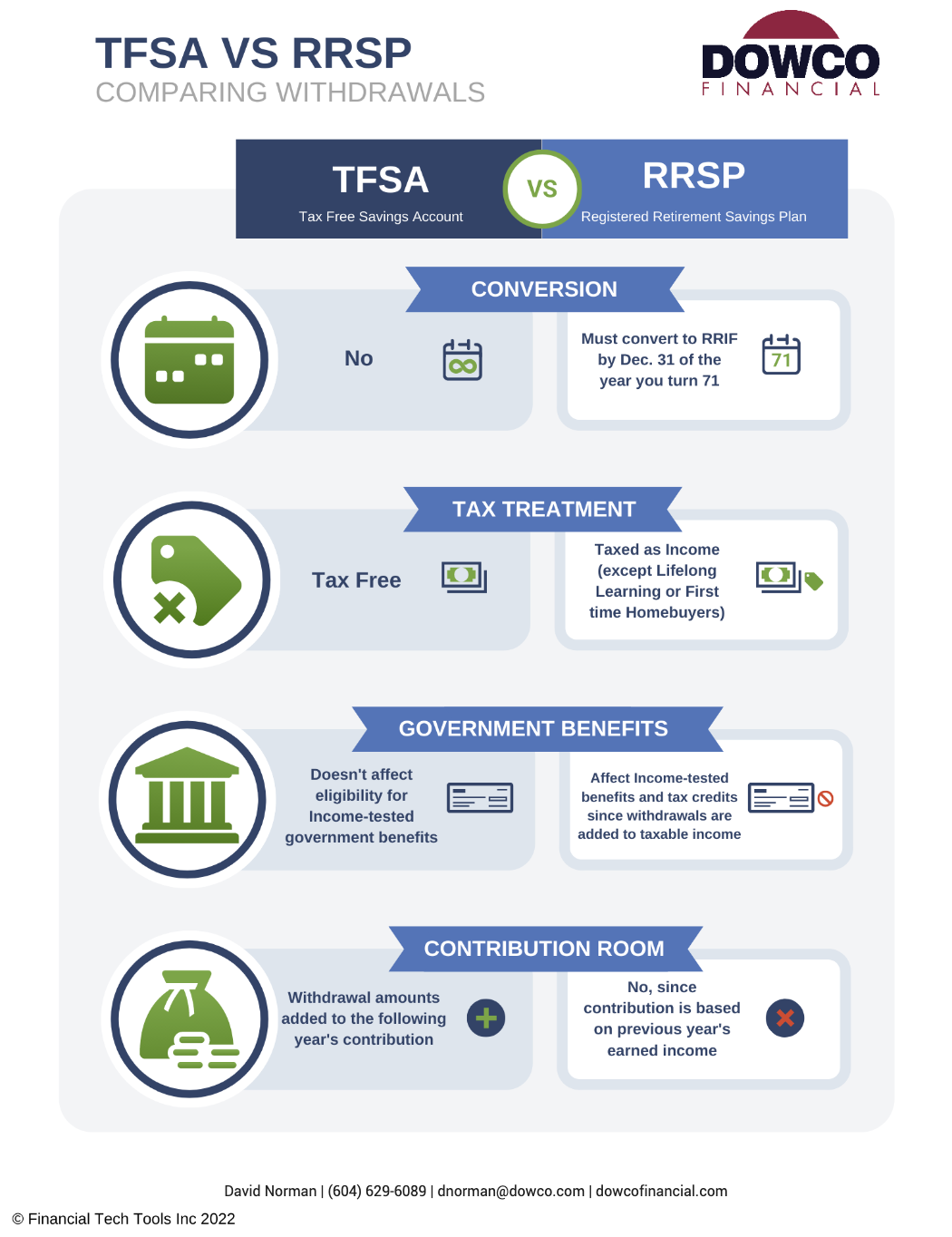

TFSA versus RRSP – What you need to know to make the most of them in 2022

TFSAs and RRSPs can be significant savings vehicles. To help you understand their differences, we have put together this article to compare:

TFSA versus RRSP – Differences in deposits

TFSA versus RRSP – Differences in withdrawals

TFSA versus RRSP – Difference in deposits

There are four main areas to focus on when comparing differences in deposits for 2022:

Contribution Room

Carry Forward

Contributions and Tax Deductibility

Tax Treatment of Growth

How much contribution room do I have?

If you have never opened a TFSA before, you can contribute up to $81,500 today. This table outlines the contribution amount you are allowed each year since TFSAs were created, including this year:

For RRSPs, the contribution limit is always 18% of your previous year’s pre-tax earnings to a maximum of $29,210. For example, if you earned $60,000 in 2021 then your contribution limit for 2022 would be $10,800 (18% x $60,000). If you earned $200,000, your contribution limit would be capped at the maximum of $29,210.

How much contribution room can I carry forward?

If you choose not to contribute to your TFSA at all one year or do not contribute the maximum amount in a year, you can indefinitely carry forward your unused contribution room. The only restrictions on this are that you must be a Canadian resident, older than 18, and have a valid social insurance number. In addition, if you make a withdrawal, the amount you withdrew is added to your annual contribution room for the following calendar year.

For an RRSP, you can carry forward your unused contribution room until the age of 71. When you turn 71, you must convert your RRSP into an RRIF. If you make a withdrawal from your RRSP, you do not open up any additional contribution room.

Contributions and Tax Deductibility

Your TFSA contributions are not tax-deductible and are made with after-tax dollars. Your RRSP contributions are tax-deductible and are made with pre-tax dollars.

Tax Treatment of Growth

One of the reasons it is essential to make both RRSP and TFSA contributions is that investment value growth is treated differently.

A TFSA is more suitable for short-term objectives like saving for a house down payment or a vacation because the investment value growth is tax-free. In addition, when you make a withdrawal from your TFSA, you will not have to pay income tax on the amount withdrawn.

The growth in an RRSP is tax-deferred, meaning you will not pay any taxes on your RRSP gains until you withdraw money from your future RRIF account; the account you convert your RRSP into at age 71. As a result, RRSPs are better suited for long-term objectives, like retirement. In addition, since you will have a lower income in retirement than when you are working, you will be in a lower tax bracket and not pay much tax on your RRIF income.

TFSA versus RRSP – Differences in withdrawals

There are four main areas to focus on when comparing differences in withdrawal for 2022:

Conversion Requirements

Tax Treatment

Government Benefits

Contribution Room

Conversion Requirements

For a TFSA, there are never any conversion requirements as there is no maximum age for a TFSA. However, if you have an RRSP, you must convert it to a Registered Retirement Income Fund (RRIF) if you turn 71 by December 31st of 2022.

Tax Treatment Of Withdrawals

One of the most attractive things about a TFSA is that all your withdrawals are tax-free! This ability to withdraw funds tax-free is why TFSAs are advantageous for short-term goals; you don’t have to worry about taxes when you take money out to pay for a house or a dream vacation.

With an RRSP, if you make a withdrawal before converting it to a RRIF, it will be taxed as income except in two cases:

The Home Buyers Plan lets you withdraw up to $35,000 tax-free, but you must pay it back within fifteen years.

The Lifelong Learning Plan lets you withdraw up to $20,000 ($10,000 maximum per year) tax-free, but you must pay it back within ten years.

How will my government benefits be impacted?

If you are withdrawing from your TFSA or RRSP, it is essential to know how your withdrawals can impact any benefits you receive from the government.

Since TFSA withdrawals are not considered taxable income, they will not impact your eligibility for income-tested government benefits.

RRSP withdrawals are considered taxable income and can affect the following:

Income-tested tax credits such as Canada Child Tax Benefit, the Working Income Tax Benefit, the Goods and Services Tax Credit, and the Age Credit.

Government benefits including Old Age Security, Guaranteed Income Supplement and Employment Insurance.

How will a withdrawal impact my contribution room?

If you make a withdrawal from your TFSA, then the amount you withdrew will be added on top of your annual contribution room for the following calendar year. However, if you withdraw money from your RRSP, you do not open up additional contribution room.

The Takeaway

RRSPs and TFSAs can both be great savings vehicles. With this in mind, understanding the differences between these two types of tax-advantaged accounts can help you better plan for future purchases and your eventual retirement.

https://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2022/02/TFSA-vs-RRSP-2022.png?time=1714369023281500Dowco Financialhttps://f5ge6f.a2cdn1.secureserver.net/wp-content/uploads/2019/12/dowcoEnfold.jpgDowco Financial2022-02-01 07:00:002022-02-01 10:21:58TFSA versus RRSP – What you need to know to make the most of them in 2022

Welcome to our 2022 financial calendar! This “at a glance” document lists important dates, including when government benefits are distributed and tax filing deadlines.

Be sure to bookmark this or add the dates listed to your personal calendar so you’re always in the loop!

Use our calendar to make sure you keep on track with your financial goals and avoid missing any critical tax or investment deadlines.

If you’re looking for help with your taxes, tax packages will be available in February 2022, so reach out to your accountant or us to book an appointment and get started on your taxes!

Important Dates

Dates to know:

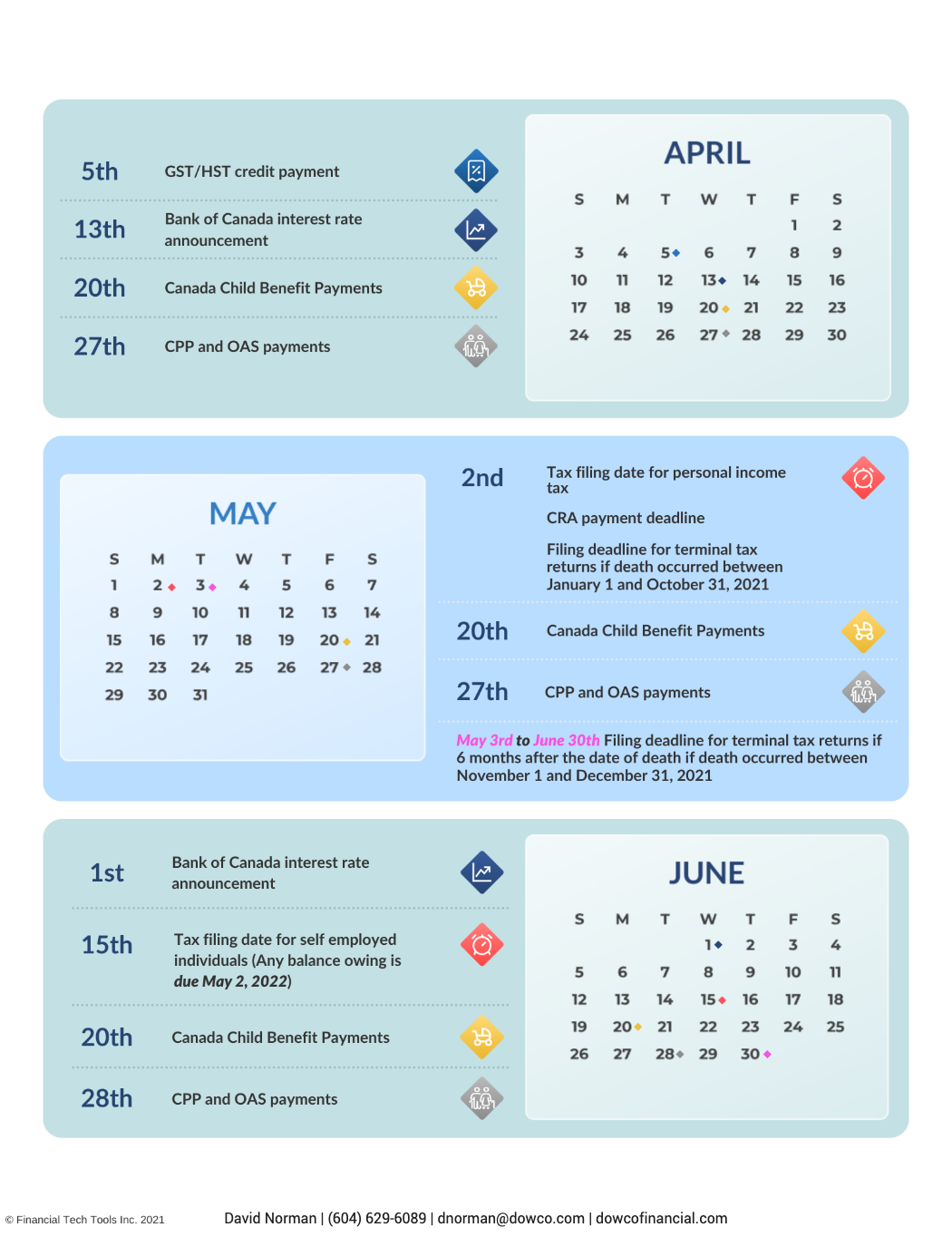

January 1 is when the contribution room for your TFSA opens again. The maximum contribution for 2022 is $6,000.

The government will issue GST/HST credit payments on January 5, April 5, July 5, and October 5.

Canada Child Benefit payments (CCB) will be issued on the following dates: January 20, February 18, March 18, April 20, May 20, June 20, July 20, August 19, September 20, October 20, November 18, and December 13.

The government will issue CPP and OAS payments on the following dates: January 27, February 24, March 29, April 27, May 27, June 28, July 27, August 29, September 27, October 27, November 28, and December 21.

The final date for your RRSP contributions to be eligible for the 2021 tax year is March 1, 2022.

Bank of Canada’s interest rate announcements will be on January 26, March 2, April 13, June 1, July 13, September 7, October 26, and December 7.

May 2, 2022, is the last day to file personal income taxes, and tax payments are also due by this date. This is also the filing deadline for final returns if death occurred between January 1 and October 31, 2021.

May 3 to June 30 – The filing deadline for final tax returns if death occurred between November 1 and December 31. The due date for the final return is six months after the date of death.

The tax deadline for all self-employment returns is June 15, 2022. Any balance owing, however, is due May 2, 2022.

The deadline for final RESP, RDSP, and TFSA contributions is December 31.

December 31 is also the deadline for 2022 charitable contributions.

December 31 is also the deadline for individuals who turned 71 in 2022 to finish contributing to their RRSPs and convert them into RRIFs.

-David-Norman-fHnp3LJtNp4ae97gn.png)