Network of Professionals

Our Network of Professionals

As a financial advisor, my primary goal is to help you achieve financial clarity. I do this by accessing a network of dedicated professionals, each bringing their unique expertise to the table. Together, we provide personalized advice and services that help you make informed decisions and secure your future.

Financial Advisor

Think of me as your financial coordinator. I help you figure out your goals, create plans to achieve them, and keep everything on track. Whether it’s planning for retirement, managing investments, or saving for a major purchase, I have access to a network of professionals who ensure every aspect of your financial life works together smoothly.

Accountant/Tax Professional

Having an accountant or tax professional in your financial network is essential for keeping your financial records in order. They handle tasks like bookkeeping, preparing financial statements, and assisting with tax planning. Their role is particularly important during tax season. They help you file your taxes accurately and on time, taking the stress out of the process. By optimizing your tax strategies and ensuring everything is reported correctly, they help you save money. Their skills are invaluable for both your immediate needs and long-term financial planning.

Investment Advisor

Investment advisors focus on building and managing investment portfolios tailored to your short-term, medium-term, and long-term goals. They thoroughly research the market, evaluate investment opportunities, and offer valuable insights to help you create a well-rounded portfolio. Whether you’re saving up for a major purchase, planning for retirement, or aiming for other financial milestones, they assist in choosing the right investment vehicles, such as RRSPs, TFSAs, RRIFs, and non-registered accounts, to support your financial stability and future needs.

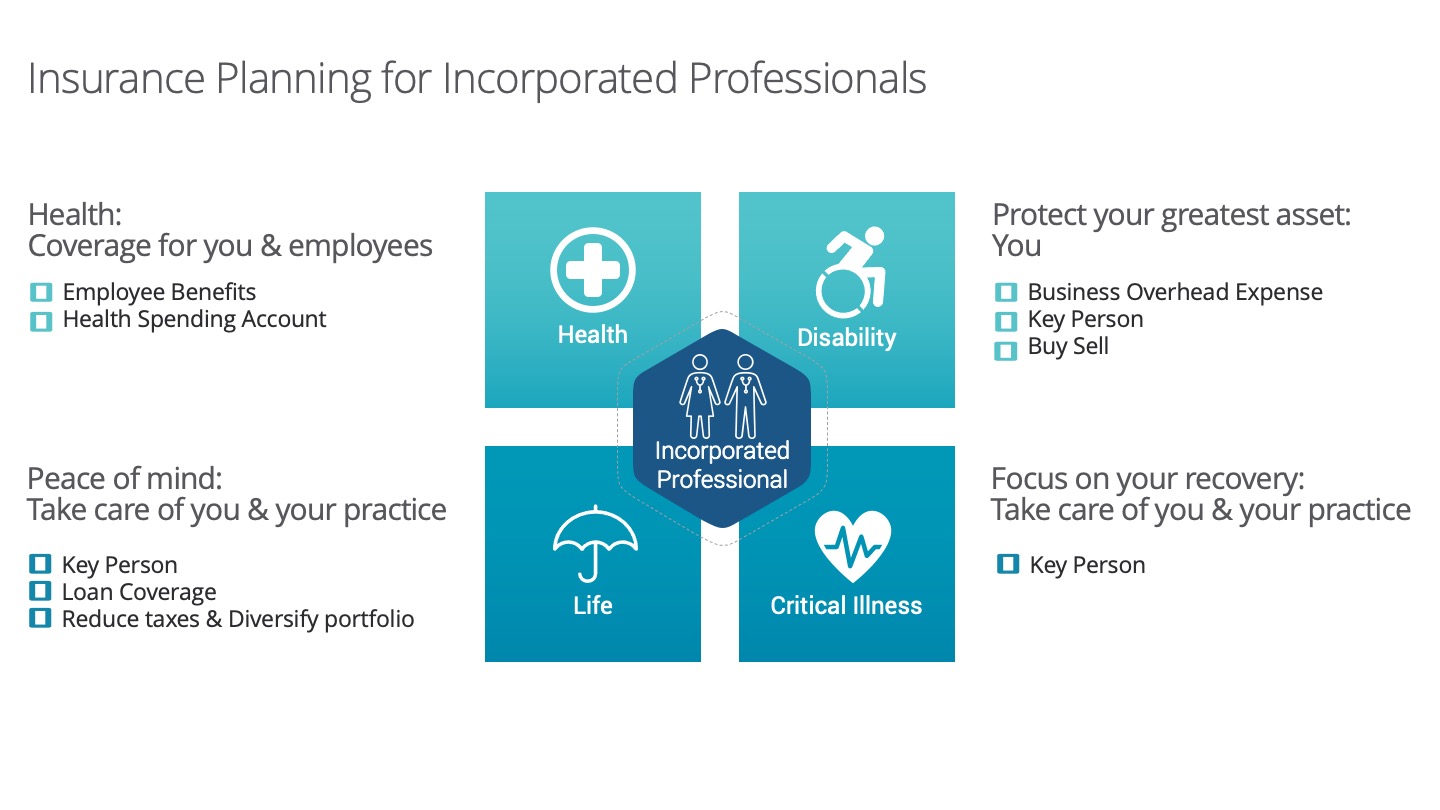

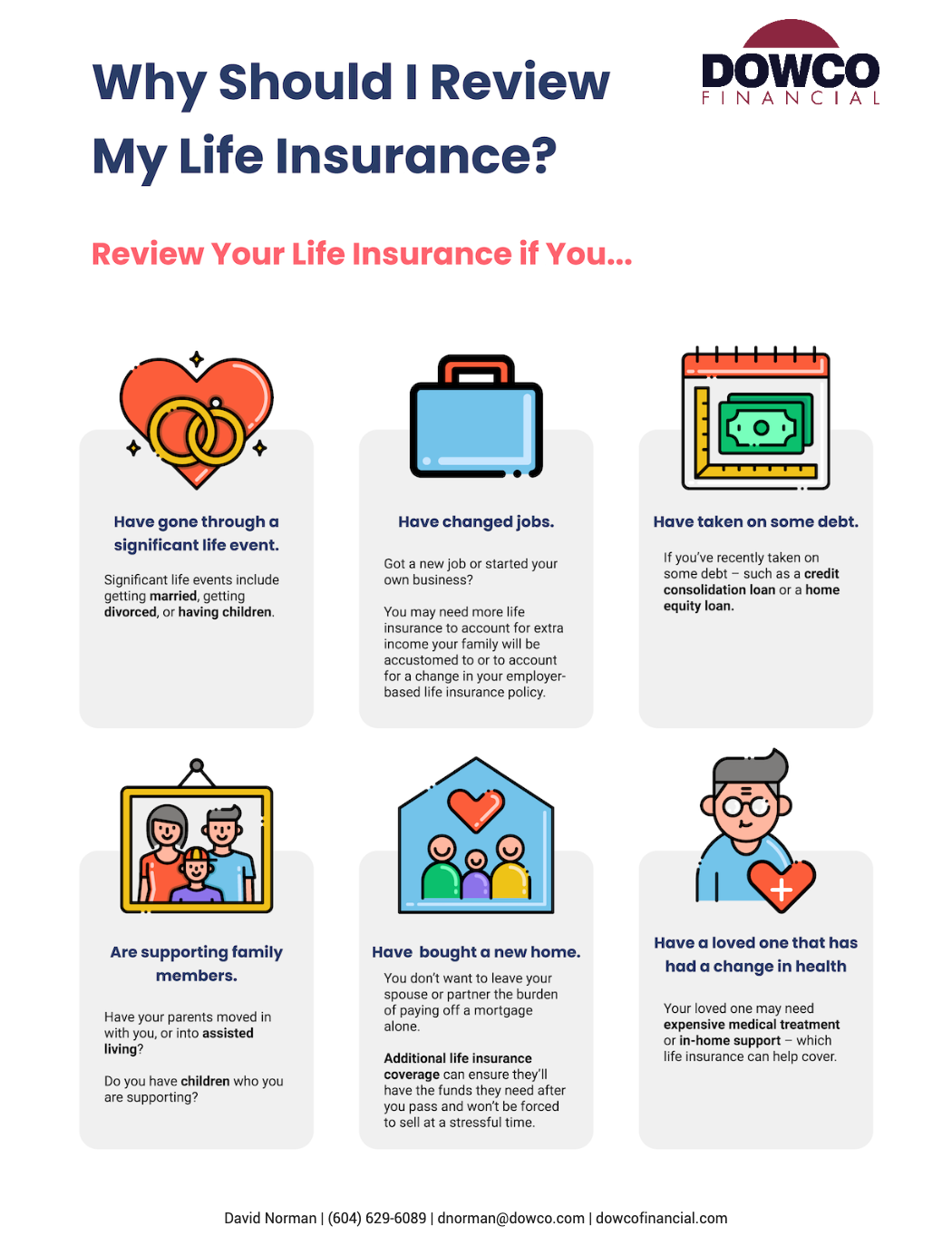

Life Insurance and Living Benefits Advisor

Life insurance and living benefits advisors are here to help you protect your greatest asset: yourself. Their job is to make sure you and your family are financially secure if unexpected events occur. These advisors walk you through different insurance options, including disability insurance, critical illness insurance, and life insurance, to find the coverage that fits your needs best. By understanding your unique situation and recommending the right policies, they provide you with peace of mind, knowing that you have a safety net in place for life’s uncertainties.

General Insurance Specialist

General insurance specialists cover a wide range of insurance needs, including auto, property, travel, and liability insurance. They assess your risks and recommend policies that provide the protection you need. Their advice helps you understand your options, compare quotes, and select the best policies to safeguard your assets, ensuring you are well-protected in various aspects of your life.

Banker

Bankers are there to help you navigate a wide range of financial services, especially when it comes to getting loans and credit products. They offer advice on securing personal loans, understanding credit options, and managing debt effectively. Whether you’re looking to finance a major purchase, consolidate debt, or build your credit, bankers provide the support and guidance you need to make informed financial decisions.

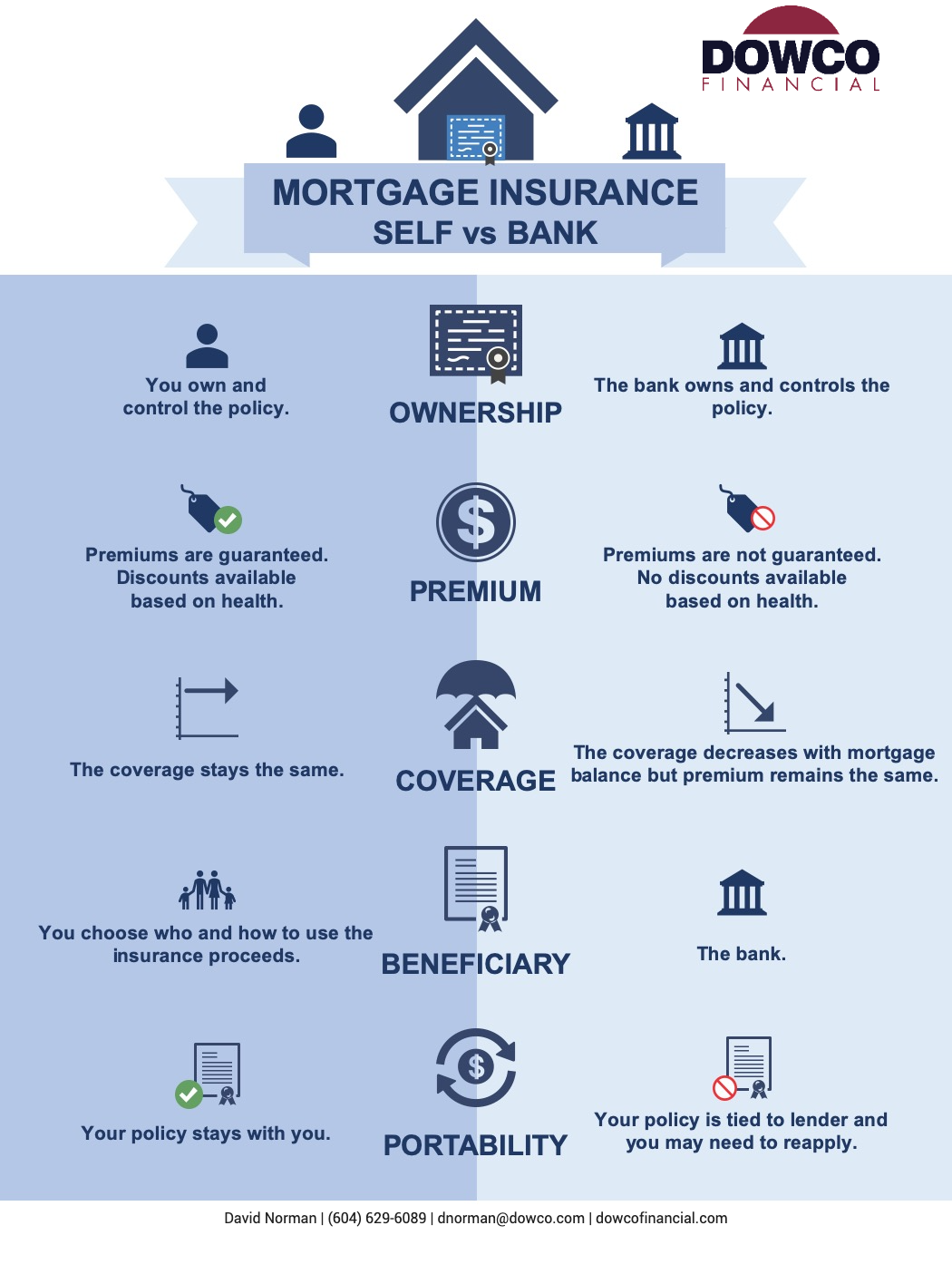

Mortgage Broker

Mortgage brokers assist you in securing financing for property purchases by accessing multiple lenders on your behalf. They assess your financial situation, compare mortgage products from various sources, and recommend the best options for you. With their ability to shop around and understand different interest rates, loan terms, and application processes, they ensure you get the best possible mortgage deal, making homeownership more accessible and affordable.

Realtor

Realtors are your go-to professionals for buying or selling property. They provide market insights, negotiate deals, and manage the legal aspects of real estate transactions. With their knowledge of local market trends and property values, realtors help you make informed decisions whether you’re purchasing a home, investing in real estate, or selling property.

Legal & Estate Professional

Legal and estate professionals play a vital role in your financial planning by handling the legal side of things, such as estate planning, wills, trusts, and probate. They make sure your assets are distributed according to your wishes and that all the necessary legal documents are properly set up. Their guidance helps you reduce estate taxes and smoothly navigate the legal processes, ensuring your wealth is transferred to future generations just as you intended.

Having a network of financial professionals is essential for achieving financial well-being. Each member brings their own expertise to address different aspects of your finances, from investments and insurance to legal and real estate matters. As your financial advisor, I act as the coordinator, ensuring that all these professionals work together seamlessly. By leveraging their combined knowledge and skills, you can gain financial clarity and know that every aspect of your financial life is taken care of.

Ready to take control of your financial future? Contact us today.